After periods of robust stock market performance, many investors feel like they might want to reduce their risk or exposure to stocks as they foresee an inevitable downturn right around the corner. They may be right, they may be wrong, they really can’t know but as a financial advisor, these are the types of concerns I need to genuinely listen to and address either by education, planning, investment adjustments, or a combination therein. As such I’d like to lay out when and how you might want to reduce risk in your portfolio.

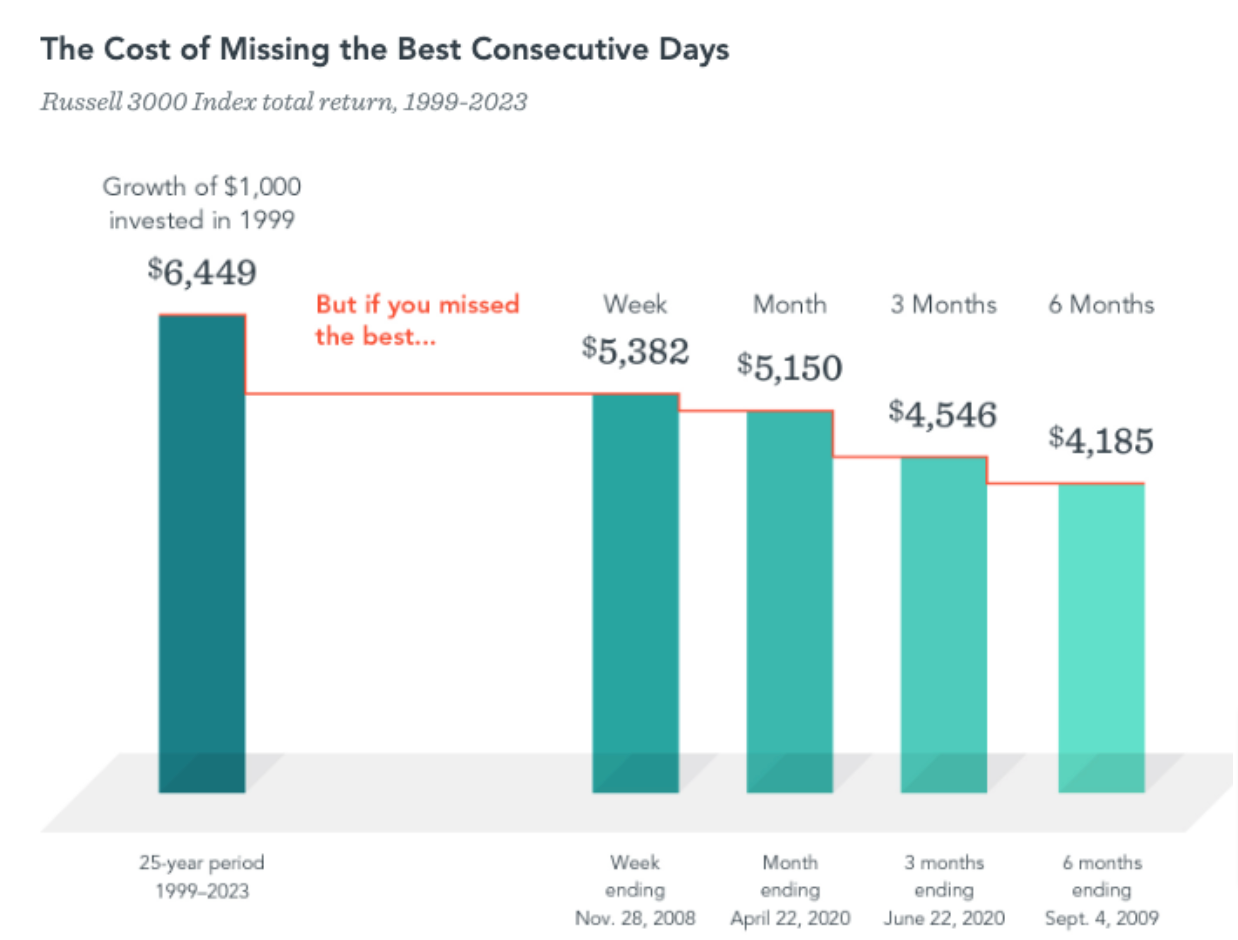

First I’d like to emphasize a reason why you should not reduce risk in your portfolio and one scenario is that your investment strategy still aligns with your long-term goals and you are fine with accepting the short-term magnitude of fluctuations of the market. Many investors have gotten out of the market because of a “feeling” which is not a way to develop or manage your financial future. Here’s why: if you miss the best periods in any given year, you can severely hinder your long-term wealth experience. These robust periods are often very short and unexpected. This next chart illustrates the potential issues with going with a feeling and the effect of missing out on robust periods.

Past performance is no guarantee of future results. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

For a better perspective, let’s put three zeroes at the end of each number from the chart above. $1,000,000 invested in the Russell 3000 index in 1999 turned into $6,449,000 by 2023. If you missed just the best week ending November 28, 2008, the portfolio would have been worth “only” $5,382,000; that’s a $1,067,000 reduction in value. That’s a lot of money to leave on the table. At the other end of the spectrum, if you decided to get on the sidelines in cash for a longer period (which often happens) and missed out on the best six-month period ending September 4, 2009, your portfolio would be $2,311,000 less valuable. I don’t think it’s a stretch to imagine the benefits an extra $2.3 million would have for your life and family goals.

Hopefully, I’ve been able to illustrate that reducing risk in a portfolio should not be driven by a feeling of what the market might do in the near future, so now we can move on to an effective strategy that investors can potentially utilize to reduce risk if needed- for valid reasons. There are always good reasons to manage risk in a portfolio and there may be very good reasons to reduce risk in a portfolio at a particular time such as: changes to your personal or financial goals, changes to your income needs, or an evolution and better understanding of your personal ability to accept risk.

This is a well-proven strategy with a lot of academic and real-world traction that we’ve implemented in our portfolio construction methodologies for many years. Having said that, it’s critical to understand how to build a bond portfolio that actually lowers risk and volatility. If you get it wrong, you might not see any benefits. This is because there are some bonds (and bond funds) that can have as much volatility as stocks such as bonds with low credit quality and longer durations. In summary, our philosophy on bond allocation as an overall risk-reduction component has three important characteristics that we usually allocate to:

- Higher Credit Quality

- Appropriate duration as projected by the current yield curve

- Global Diversification

For investors concerned about aligning their values with investment options, there will most likely be a need to adjust strategies slightly to deliver a higher probability that you are not investing in companies that are not aligned with your conservative values. The goal of course is to make these adjustments while maintaining the opportunity for growth and the reduction of risk as necessary.

2024 Q1 Review

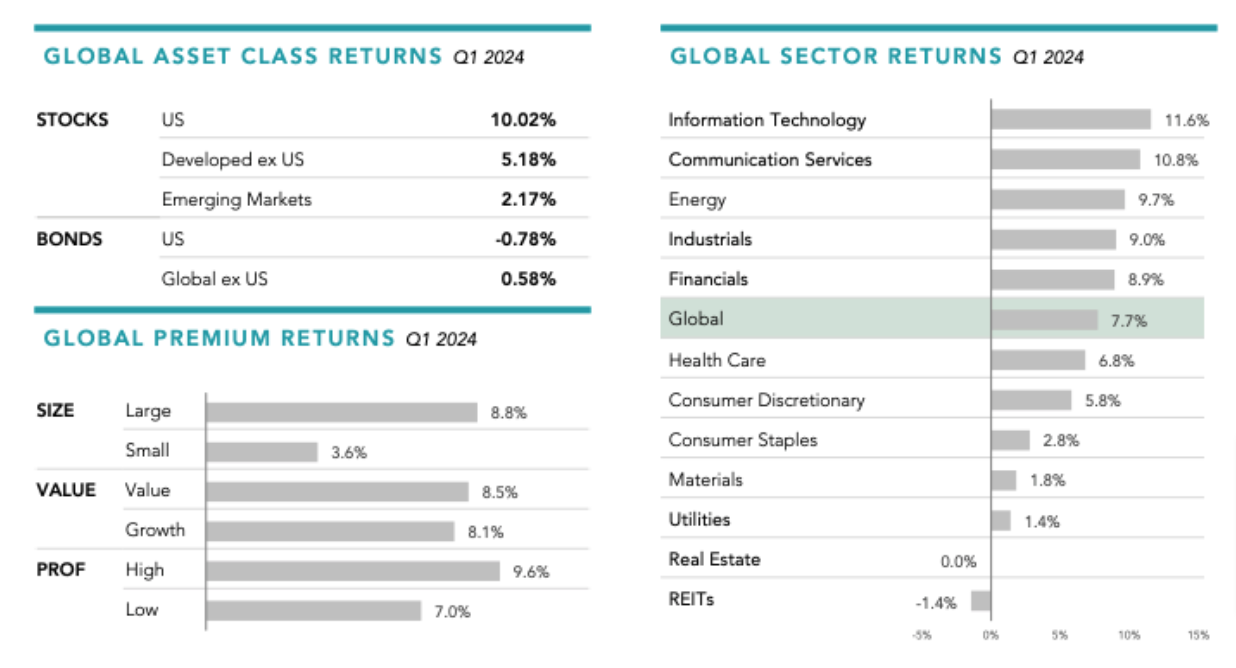

Global stocks had an impressive start to the year, returning 8% in the first quarter. The prospect of an AI-driven productivity boom drove stocks higher, especially in the US, outweighing areas of uncertainty such as higher-for-longer interest rates and upcoming US elections.

Japan made headlines as the Nikkei reached new record highs for the first time since 1989. And major US indices, including the Russell 3000 and S&P 500 Index, ended the quarter at all-time highs. IT and Communication Services stocks led the stock market gains but it wasn’t concentrated in the “Magnificent 7” names that led the US market last year. While Nvidia, Microsoft, Meta and Amazon all contributed to market returns, both Apple and Tesla detracted. REITs were the only sector to post negative returns for the quarter, falling after a strong fourth quarter last year.

Globally, value stocks trailed growth stocks and small caps trailed large caps. However, profitability offered a ballast against these negative premiums, as stocks with higher profitability generally outperformed their lower profitability counterparts.

Past performance is no guarantee of future results. This information is provided for registered investment advisors and institutional investors and is not intended for public use. Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission. Market segment (index representation) as follows: US Stock Market (Russell 3000 Index), Developed ex US Stocks (MSCI World ex USA IMI Index [net div.]), Emerging Markets (MSCI Emerging Markets IMI Index [net div.]), US Bond Market (Bloomberg US Aggregate Bond Index), and Global Bond Market ex US (Bloomberg Global Aggregate ex-USD Bond Index [hedged to USD]), Global Stock Market (MSCI All Country World IMI Index [net div.]). Sector returns are derived by Dimensional using constituent data from the MSCI All Country World IMI Index. Returns for specific securities are sourced from the MSCI All Country World IMI Index using daily security returns. Securities without a GICS sector are excluded. Sectors are classified according to GICS Industry code. GICS was developed by and is the exclusive property of MSCI and S&P Dow Jones Indices LLC, a division of S&P Global. S&P data © 2024 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2024, all rights reserved. Bloomberg data provided by Bloomberg. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio. References to specific company securities should not be construed as a recommendation or investment advice. Global Premium Returns are computed from MSCI All Country World IMI Index published security weights and Dimensional computed security returns and Dimensional classification of securities based on size, value, and profitability parameters. Within the US, Large Cap is defined as approximately the largest 90% of market capitalization in each country or region; Small Cap is approximately the smallest 10%. Within the non-US developed markets, Large Cap is defined as approximately the largest 87.5% of market capitalization in each country or region; Small Cap is approximately the smallest 12.5%. Within emerging markets, Large Cap is defined as approximately the largest 85% of market capitalization in each country or region; Small Cap is approximately the smallest 15%. Designations between value and growth are based on price-to-book ratios. Value is defined as the 50% of market cap with the lowest price-to-book ratios by size category and growth is the highest 50%. Profitability is measured as operating income before depreciation and amortization minus interest expense scaled by book. High profitability is defined as the 50% of market cap with the highest profitability by size category and low profitability is the lowest 50%. REITs and utilities, identified by GICS code, and stocks without size, relative price, or profitability metrics are excluded from this analysis. Countries not in the Dimensional investable universe are excluded from the analysis. Their performance does not reflect the expenses associated with the management of an actual portfolio. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. Named securities may be held in accounts managed by Dimensional.

Morgan H Smith Jr. is an investment advisor with Constitution Wealth. Constitution Wealth is a registered investment adviser in Wyoming. Constitution Wealth is registered with the Securities and Exchange Commission (SEC). Registration of an investment advisor does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the commission. Constitution Wealth only transacts business in states in which the firm is properly registered or is excluded or exempted from registration. A copy of Constitution Wealth’s current written disclosure brochure filed with the SEC, which discusses among other things, Constitution Wealth’s business practices, services, and fees, is available through the SEC’s website at www.adviserinfo.sec.gov.

Please note, the information provided in this document is for informational purposes only and investors should determine for themselves whether a particular service or product is suitable for their investment needs. Please refer to the disclosure and offering documents for further information concerning specific products or services.

Any hypothetical, backtested performance has been provided for illustrative purposes only, and is not necessarily, and does not purport to be, indicative, or a guarantee, of future results or the adviser’s skill. Hypothetical, backtested performance does not represent actual performance. The results are prepared by retroactive application of a model, with the benefit of hindsight, and actual results may vary substantially. The preparation of such information is based on underlying assumptions, and does not represent the actual performance of any fund, portfolio, or investor, it is subject to risk and limitations that are not applicable to non-hypothetical performance presentations. Although advisor believes any hypothetical, backtested performance calculations described herein are based on reasonable assumptions, the use of different assumptions would produce different results. For the foregoing and other similar reasons, the comparability of hypothetical, backtested performance to the prior (or future) actual performance of a fund is limited, and prospective investors should not unduly rely on any such information in making an investment decision.

Nothing provided in this document constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation or an offer to sell (or solicitation of an offer to buy) securities in the U.S. or in any other jurisdiction.

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions; changing levels of competition within certain industries and markets; changes in interest rates; changes in legislation or regulation; and other economic, competitive, governmental, regulatory, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties, and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Constitution Wealth or any of its affiliates or principals or any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events, or any other circumstances. All statements made herein speak only as of the date they were made.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends, and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular hedge fund.